The Ultimate Checklist for International Ecommerce Entrepreneurs Incorporating a Business in the US

Introduction

Did you know that around 80% of the US population prefers shopping online? Thanks to online shoppers, the e-commerce market in the country is all set to reach a new peak of $1.9 trillion by 2029. This staggering value suggests a massive increase from $1.119 trillion in 2023, making the digital marketplace a goldmine for entrepreneurs. Therefore, starting an online retail business in the United States can be an exhilarating venture with significant expansion and income potential.

However, navigating the complex US accounting and bookkeeping statutes can be particularly daunting for foreign entrepreneurs. Mastering these financial regulations' intricacies is pivotal to constructing a sturdy foundation for your e-commerce business to withstand the test of time. With e-commerce sales projected to account for 22.6% of all retail sales by 2027, comprehending these principles is more important than ever.

This comprehensive manual offers a meticulously detailed checklist to help you understand and adhere to these regulations, ensuring your online retail operation thrives within the highly competitive US commercial sphere.

Whether you're managing the nuanced complexities of sales tax calculations or developing an optimized bookkeeping infrastructure, this guide is equipped to supply you with the knowledge required to achieve success. Let us embark on this journey together and transform the staggering numbers into a prosperous reality for your business.

Checklist 1: GAAP Compliance

The Generally Accepted Accounting Principles (GAAP) are fundamental for financial reporting in the United States. It revolves around the following fundamental rules:

Accrual accounting techniques: GAAP employs accrual accounting, which records earnings when services or goods are sold, not when payment is received. Direct expenses related to goods sold are recorded at the time of sale, while indirect expenses are recorded when they are paid.

Depreciation and capital expenditures: The costs of acquiring significant assets are spread out over the entire lifespan of the asset. For instance, an asset with a 10-year lifespan depreciates 10% over ten years.

Reporting of historical costs: Certain assets, such as property, equipment, and facilities, are recorded based on their original purchase prices rather than their current market values.

Reporting of bad debts: Companies with substantial amounts owed by customers or accounts receivable must acknowledge the possibility that some or all of that money may not be collected, resulting in lost revenue.

For global entrepreneurs, adhering to GAAP is crucial in building confidence among investors, customers, and regulatory bodies. A prominent example is the Enron scandal, where failure to comply with GAAP led to one of the largest financial frauds in history.

The Enron Scandal and Its Violation of GAAP Principles

The scandal involving Enron considered one of the most infamous cases of corporate deception in history, was brought to public attention in 2001. Enron, a company specializing in energy based in Houston, Texas, engaged in widespread fraudulent accounting practices to conceal its financial losses and boost its reported earnings, misleading investors and stakeholders.

The deceitful actions carried out by Enron went against numerous key GAAP principles, which included:

Recognition of Revenue: Enron utilized the "mark-to-market" accounting method to record potential future profits from long-term contracts as immediate income, significantly inflating its earnings.

Entities Off the Balance Sheet: The company established intricate partnerships off the balance sheet to mask its debts and overstate the value of its assets, giving investors a false impression of its actual financial status.

Complete Disclosure: Enron neglected to offer clear and honest disclosures in its financial reports, obscuring its monetary challenges' true nature and scope.

The scandal involved a chain of incidents that led to the financial ruin of the Enron Corporation in 2001 and the disbandment of Arthur Andersen LLP, which was once a major auditing and accounting firm globally.

The downfall of Enron, a company with assets exceeding $60 billion, included a colossal bankruptcy declaration in U.S. history. It triggered extensive discussions and laws to enhance accounting rules and methodologies with long-lasting impacts on the economic sector.

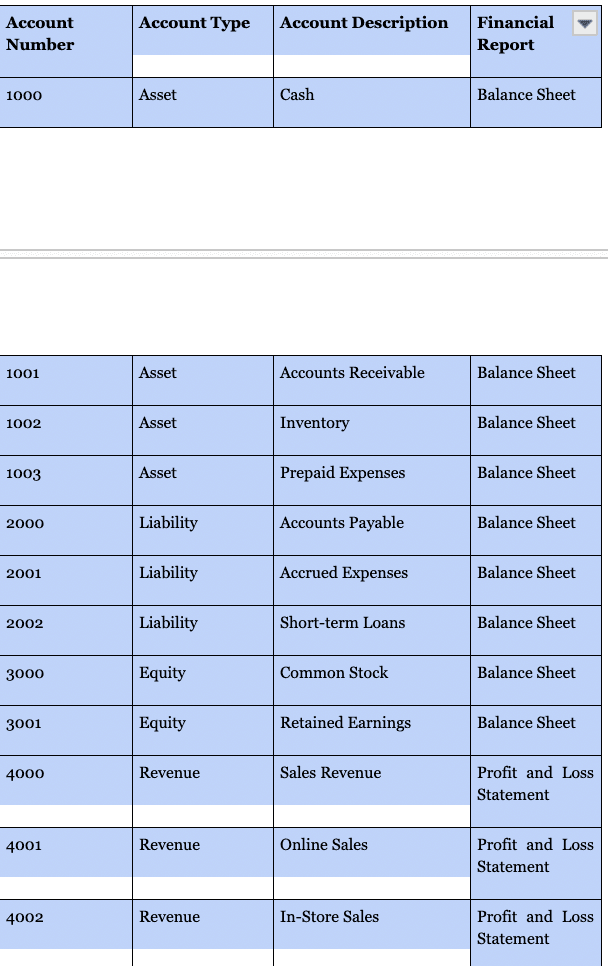

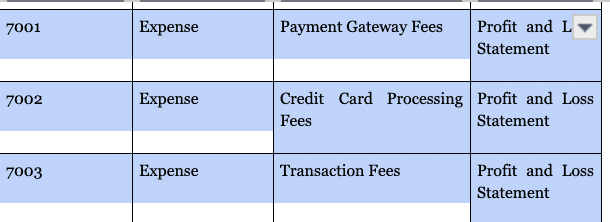

Checklist 2: Creating a Chart of Accounts

A chart of accounts catalogs the diverse ledger accounts for a business systematically. Organizing transactions into financial groupings streamlines management and reporting, clarifying the enterprise's monetary flows. For ecommerce specifically, essential classes involve sales revenue, cost of goods sold (COGS), shipping expenses, and merchant fees. With a rationally ordered chart, reporting and examining fiscal performance becomes easier.

A four-digit system is commonly used by e-commerce businesses to create their chart of accounts. Here’s an example:

Checklist 3: Implementing Internal Controls

Establishing internal controls is pivotal for preventing fraud and confirming the authenticity of your fiscal reporting. Key measures involve:

separating responsibilities between different personnel

carrying out habitual reconciliations

instituting authorization procedures for dealings

Internal controls safeguard your business from financial inconsistencies and heighten your financial statements' credibility. Furthermore, internal controls ensure employees maintain proper operating techniques and adhere to compliance standards.

The Sarbanes-Oxley Act of 2002, implemented after the Enron scandal, underscores the necessity of internal controls in guaranteeing corporate responsibility. Moreover, consistent oversight helps ensure that transactions are correctly recorded and potential issues are promptly recognized and addressed.

Checklist 4: Legal and Regulatory Considerations

Understanding the legal and regulatory environment to run your online retail business lawfully and effectively is essential. This section will outline important factors to consider to ensure compliance.

Business Structure

Selecting the proper business structure for your online retail project is very important. Options include:

Sole Proprietorship

Partnership

Limited Liability Company (LLC)

S Corporation

Many online retail startups prefer an LLC structure for its flexibility and protection against liability.

Licenses

Acquiring the necessary licenses and permits to legally operate your online retail business. This might involve obtaining a general business license, a sales tax permit, and any specific permits required by your state or area of operation.

Privacy Regulations

Online retail businesses must adhere to data security and privacy regulations, like the General Data Protection Regulation (GDPR). Failure to abide by privacy laws can result in hefty financial penalties and harm your company's reputation. For example, in March 2020, a class action lawsuit was filed against the video conferencing service Zoom for allegedly breaching the privacy of millions of users by providing personal data to Facebook, Google, and LinkedIn.

Checklist 5: Tax Compliance and Reporting

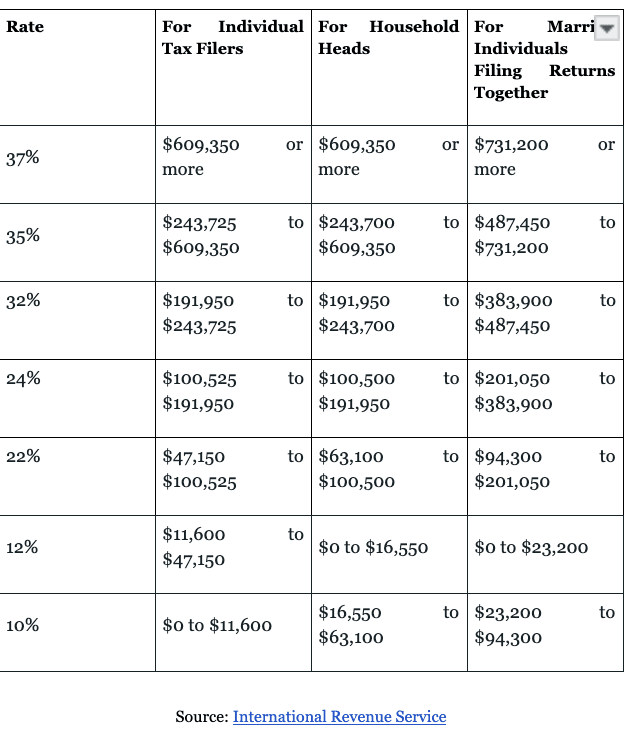

As an international entrepreneur, you must disclose all connected U.S. business earnings on federal Form 1120-F and settle appropriate corporate taxes following American accounting regulations. You are eligible to request deductions for regular and essential business costs. America follows a progressive tax scale, which means that higher tax rates apply to individuals with a higher level of income.

Federal Income Tax Brackets in the US 2024

Your company might also have to document earnings and expenditures assigned to specific states where you have a sales tax connection. Many states employ a distribution formula based on the percentage of your sales, assets, and workforce present in that state. It is also important to carefully plan transactions with associated foreign entities to comply with transfer pricing guidelines.

The IRS pays close attention to improper manipulation of profits and losses among foreign-linked businesses. Tax agreements between nations offer advantageous safeguards, like lowered withholding rates on payments subject to reporting criteria such as FATCA.

Checklist 6: Preparing Financial Statements

Preparing financial reports is crucial for evaluating the performance of your business and making well-informed choices. This segment discusses the main financial reports that you should compile regularly.

Balance Sheet

It offers a glimpse of your business's financial state at a particular moment. It encompasses assets, debts, and ownership. Consistently preparing and examining your balance sheet allows you to keep track of your financial well-being, evaluate liquidity, and confirm that your business is in a secure position.

Profit and Loss Statement

Also identified as the income statement, the profit and loss report condenses your business's earnings and expenses during a specific duration. It provides insights into profitability and operational effectiveness. Utilize the income statement to analyze patterns, pinpoint areas for expense reduction, and make wise business judgments.

Cash Flow Statement

The cash flow statement traces the influx and outflow of cash in your business throughout a period. It aids in comprehending your liquidity and handling cash proficiently. Regularly assessing cash flow reports is crucial for upholding financial stability, planning future costs, and ensuring your business can fulfill its responsibilities.

Need Help To Incorporate Your Ecommerce Business: Contact Samscashflow Agency

Looking for effective support to streamline your business’ cash flow statement? Book a call to SamsCashFlow today. As one of the leading ecommerce tax accountants and bookkeeping experts, we can help you achieve the right financial clarity.

Appendices:

Appendix 1

Rate ; For Individual Tax Filers ; For Household Heads ; For Married Individuals Filing Returns Together

37% ; $609,350 or more ; $609,350 or more ; $731,200 or more

35% ; $243,725 to $609,350 ; $243,700 to $609,350 ; $487,450 to $731,200

32% ; $191,950 to $243,725 ; $191,950 to $243,700 ;$383,900 to $487,450

24% ; $100,525 to $191,950 ; $100,500 to $191,950 ; $201,050 to $383,900

22% ; $47,150 to $100,525 ; $63,100 to $100,500 ;$94,300 to $201,050

12% ; $11,600 to $47,150 ; $0 to $16,550 ; $0 to $23,200

10% ; $0 to $11,600 ; $16,550 to $63,100 ; $23,200 to $94,300

Appendix 2

Account Number ; Account Type ; Account Description ; Financial Report

1000 ; Asset ; Cash ; Balance Sheet

1001 ; Asset ; Accounts Receivable ; Balance Sheet

1002 ; Asset ; Inventory ; Balance Sheet

1003 ; Asset ; Prepaid Expenses ; Balance Sheet

2000 ; Liability ; Accounts Payable ; Balance Sheet

2001 ; Liability ; Accrued Expenses ; Balance Sheet

2002 ; Liability ; Short-term Loans ; Balance Sheet

3000 ; Equity ; Common Stock ; Balance Sheet

3001 ; Equity ; Retained Earnings ; Balance Sheet

4000 ; Revenue ; Sales Revenue ; Profit and Loss Statement

4001 ; Revenue ; Online Sales ; Profit and Loss Statement

4002 ; Revenue ; In-Store Sales ; Profit and Loss Statement

5000 ; Cost of Goods Sold ; Cost of Goods Sold ; Profit and Loss Statement

5001 ; Cost of Goods Sold ; Purchase of Inventory ; Profit and Loss Statement

5002 ; Cost of Goods Sold ; Inventory Adjustments ; Profit and Loss Statement

5003 ; Cost of Goods Sold ; Direct Labor Costs ; Profit and Loss Statement

6000 ; Expense ; Shipping Expenses ; Profit and Loss Statement

6001 ; Expense ; Shipping Supplies ; Profit and Loss Statement

6002 ; Expense ; Shipping Labor ; Profit and Loss Statement

6003 ; Expense ; Shipping Insurance ;Profit and Loss Statement

6004 ; Expense ; Freight Charges ; Profit and Loss Statement

7000 ; Expense; Merchant Fees ; Profit and Loss Statement

7001 ; Expense ; Payment Gateway Fees ; Profit and Loss Statement

7002 ; Expense ; Credit Card Processing Fees ; Profit and Loss Statement

7003 ; Expense ; Transaction Fees ; Profit and Loss Statement